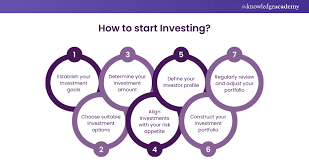

Introduction: Why Early Investing Is a Career Advantage

Many professionals believe investing is something to focus on later—after income increases, careers stabilize, or responsibilities feel lighter. From a CEO’s perspective, this belief is one of the most costly misconceptions in personal finance. The most powerful advantage in investing is not intelligence, access, or even capital. It is time.

Starting to invest early in your career is not about becoming wealthy overnight. It is about building habits, discipline, and optionality that compound alongside professional growth. Early investing shapes how you think about money, risk, and long-term decision-making. These skills are as valuable as technical expertise or leadership ability.

This article explores why starting early matters, what lessons CEOs learn from early investing, and how young professionals can approach investing with clarity and confidence.

1. Time Is the Ultimate Force Multiplier

In business, CEOs understand leverage. In investing, time is the most reliable form of leverage available.

Compounding rewards consistency over long periods. Even modest investments, when started early, can outperform larger investments made later. This is not theory—it is mathematics reinforced by behavior.

Early in your career, you may not have significant capital, but you possess something far more valuable: a long runway. Each year invested early has more time to grow, recover from volatility, and benefit from reinvestment.

From a CEO’s perspective, starting early is a strategic decision that maximizes return on effort.

2. Investing Early Builds Financial Discipline

Discipline is a defining trait of effective leaders. Investing early trains discipline long before stakes become large.

By committing to regular investing, young professionals learn to prioritize long-term goals over short-term consumption. They learn to budget, to delay gratification, and to stay consistent regardless of market conditions.

These habits often matter more than investment selection. CEOs know that strong systems outperform occasional brilliance. Early investing helps establish those systems when behavioral patterns are still forming.

3. Small Amounts Reduce Emotional Pressure

One advantage of investing early with smaller amounts is reduced emotional intensity. Losses feel manageable, and gains feel educational rather than intoxicating.

This environment is ideal for learning. Early investors can observe market behavior, volatility, and their own emotional reactions without risking financial stability.

CEOs value low-cost learning. Early investing provides real-world experience that no book or course can replicate.

4. Learning Markets Before Responsibility Increases

As careers progress, responsibilities multiply—families, mortgages, businesses, and leadership roles. Decision-making becomes more complex and risk tolerance narrows.

Investing early allows individuals to develop market literacy before pressure increases. They learn how different assets behave, how cycles unfold, and how patience is rewarded.

From a CEO’s perspective, experience gained early becomes strategic confidence later.

5. Early Investing Shapes a Long-Term Mindset

One of the most valuable lessons of early investing is long-term thinking. Markets punish impatience and reward consistency.

Young professionals who invest early learn to think in years rather than weeks. This mindset aligns closely with executive leadership, where sustainable success depends on long-term vision.

CEOs recognize that leaders who think long term make better decisions across all areas of life.

6. Income Growth Amplifies Early Habits

Career growth typically leads to higher income. When investing habits are established early, increased income accelerates results rather than creating confusion.

Instead of asking how to start investing later, early investors simply scale what already works. This reduces friction and decision fatigue.

From a CEO’s standpoint, this is operational efficiency applied to personal finance.

7. Risk Tolerance Is Higher Earlier

Early in a career, individuals generally have greater capacity to absorb volatility. There is more time to recover from downturns and fewer immediate financial obligations.

This does not mean reckless behavior is justified. It means that a long-term, growth-oriented approach is more feasible.

CEOs understand that appropriate risk, taken early and managed responsibly, often leads to superior outcomes.

8. Investing Early Encourages Ownership Thinking

Investing introduces the concept of ownership. Rather than seeing money solely as income, early investors begin to see capital as a productive asset.

Ownership thinking is central to executive leadership. CEOs focus on value creation, not just compensation.

By investing early, professionals train themselves to think like owners rather than consumers.

9. Simplicity Beats Perfection

Young investors often feel pressure to find the perfect strategy. CEOs know that perfection is unnecessary and often counterproductive.

Simple, consistent investing approaches outperform complex strategies that require constant adjustment. Early investing should focus on fundamentals, diversification, and discipline.

Starting matters more than optimizing.

10. Automation Creates Consistency

Automating investments early removes reliance on motivation. Regular contributions become default behavior.

CEOs design systems that function regardless of mood or distraction. Automation applies this principle directly to investing.

Consistency, not intensity, drives long-term success.

11. Early Mistakes Become Valuable Lessons

Mistakes made early are often inexpensive and highly educational. They shape judgment and improve future decision-making.

CEOs value failure when it occurs early and informs better strategy later. Early investing provides this learning curve with relatively low cost.

12. Confidence Grows With Experience

Confidence in investing does not come from predictions; it comes from experience.

Early investors develop confidence through cycles—both positive and negative. This confidence reduces emotional decision-making later in life.

From a CEO’s perspective, calm decision-making under uncertainty is a critical leadership skill.

13. Early Investing Supports Career Flexibility

Financial progress creates optionality. Optionality allows professionals to take calculated career risks, pursue opportunities, or withstand transitions.

CEOs understand that freedom to choose is a form of power. Early investing supports that freedom.

14. Aligning Values With Capital Early

Starting early allows investors to reflect on what they want their money to support. Ethical considerations, sustainability, and long-term impact become part of decision-making.

This alignment strengthens integrity and purpose.

Conclusion: Start Early, Lead Better

Starting to invest early in your career is not just a financial decision—it is a leadership decision. It builds discipline, long-term thinking, emotional resilience, and ownership mindset.

From a CEO’s perspective, early investing creates professionals who are more strategic, confident, and prepared for responsibility.

The most successful leaders rarely wish they had started investing later. They wish they had started sooner.

The best time to invest was yesterday. The second-best time is now.

Word Count:

481

Summary:

The time to start investing is when you are young. If you have a college degree and you start investing immediately after you graduate and get your first job, it is possible to retire as a millionaire. Find an employer that will match your 401K contribution.

Keywords:

investment, 401K, retirement, millionaire

Article Body:

You�re young, you just landed a new job and you�re going to be getting a decent paycheck. You also have bills to pay and there are also a few items that you�ve always wanted so now you can finally afford them.

Investing for your retirement may be the last thing on your mind at the start of a new career. Take some advice from those with a little more experience: Start investing early in your career. Start from day one and you will never miss that money you�re setting aside. If your company has available a 401-K or a TSP program, jump on the band wagon immediately. If you don�t have these programs at your disposal, you can still start an IRA and the concepts stated here are applicable as well.

It really does it make a difference when you start contributing. It is important to invest in your retirement account early in your career for two reasons. First, if you�re fortunate to receive matching contributions, you don’t want to miss out on those added contributions that are a significant part of your retirement benefit. Second, the longer contributions stay in your account, the more you stand to gain. Your money makes money in the form of earnings, and those earnings in turn make money, and so on. This is what is known as the “miracle of compounding.” As money grows in your account over time, the proportion resulting from earnings will become larger compared to the proportion resulting from contributions.

The size of your account balance is going to depend on how much you (and your company if they match funds up to a certain percentage) contribute to your account and how your account grows as a result of earnings on your investments. To get an idea of what your retirement account could be in the future, look at the following projections.

Assume that you are an employee eligible for organizational contributions, that you are earning $28,000 each year, and that you receive no future salary increases. You choose to save 5 percent of basic pay each pay period; therefore you receive total organizational contributions of 5 percent. The growth projections below are for an assumed annual rate of return of 7 percent on your investments.

After five years your account balance would be almost $17,000; after ten years your balance would increase to $40,000; and after contributing for twenty years, your account would have a balance of $122,000. Clearly your balance would continue to increase each year. If you contributed for forty years, which is fathomable if you start a job at 23 and want to retire at age 63, your account balance would be $615,000. That�s over half a million dollars folks! Just from contributing 5% of your income from the day you start work!

Looking at the numbers, it�s hard to imagine why someone wouldn�t start investing immediately!

Tinggalkan Balasan